Help! I have multiple pensions and don't know what to do

For most of us, our pension is our second-biggest asset after our homes. But over our careers we could accumulate a number of pension pots and lose track of how they are invested. Could putting them in one place give you better control over how they are invested to make sure they are on track to meeting your long-term financial goals?

It’s essential we review our pension savings regularly. For most of us, our pension is our second-biggest asset after our homes and making the most of our pension savings could have a significant impact on our happiness in retirement. Getting it right could mean achieving a higher income, or the potential of an earlier retirement date. If we find a shortfall, the need for action is clear.

According to global recruitment partners BPS world [1], staff typically stay with one employer for an average of 4.5 years. With government legislation aiming to increase the number of employees saving for retirement, most of us can expect to be auto-enrolled into a new plan every time we start a new job. Over a working life the average UK worker is therefore likely to have ten jobs and therefore ten pensions. Separate research by the professional services network Deloite Global found millennials change jobs every two years [2].

Accumulating numerous workplace pensions from different employers can make things complicated when creating a coherent retirement strategy. Especially when you consider that nearly a fifth of us have lost track of at least one pension [3]. The government offers a free pension tracing service if you’re struggling with this.

Consolidating your pensions – that is, transferring them under one roof – could make things easier to manage, help you target your long-term goals better, and reduce costs, depending on the type of pension and your individual circumstances.

The dangers of a laissez-faire approach

Nearly a fifth of us have lost track of at least one pension.

When we join our employer’s pension scheme we may be offered a choice of investments, but as very few of us are investment gurus, the temptation is to plump for the default option. There is nothing intrinsically wrong with that: it is usually designed to meet the broad needs of most of the scheme’s members. But that doesn’t necessarily mean it meets your specific long-term goals.

But we move on and our needs change, and over time the historical investment policy and strategy might no longer be appropriate. Furthermore, there’s a danger these left-behind plans end up languishing in expensive, poorly performing funds.

The impact of high charges on your pension schemes

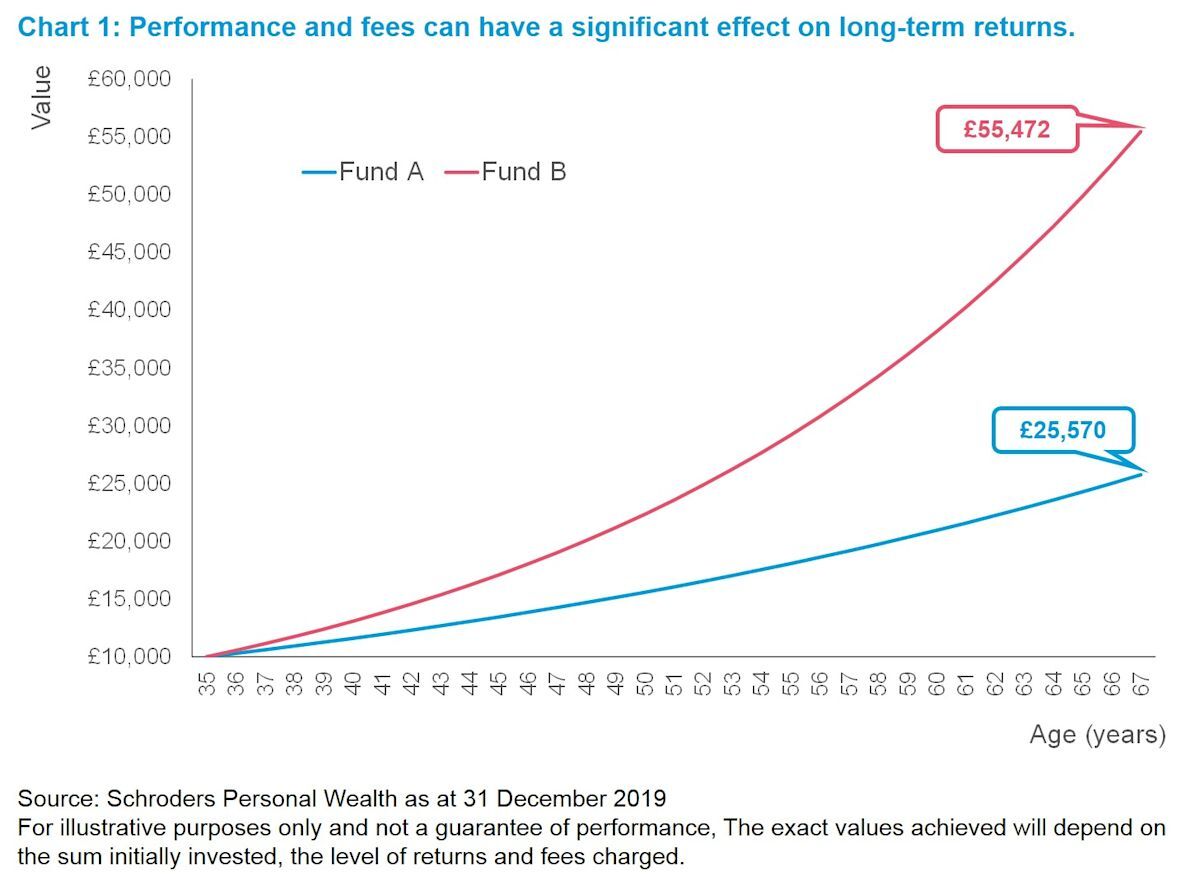

The negative effect of high charges and poor fund performance shouldn’t be underestimated either. Take a 35-year-old investing £10,000 in Fund A which returns a constant 5% per annum in performance, but charges 2% a year. At the new state retirement age of 67 that pot will be worth £25,750. That same £10,000 invested in Fund B returning 7% a year with a 1.5% annual charge, would be worth £55,472. More than double the value.

This is illustrated in Chart 1, below.

Just switching to another fund can’t guarantee better returns in the future, however, although transferring to a new plan could provide you with more investment choices at lower fees. You should also consider your appetite for accepting losses, and balance any potential returns after fees against the risks of a particular investment strategy, to decide what is best for your individual circumstances.

The mechanics of pension consolidation

If considering pension consolidation as an option, there are two routes you could take:

- Roll all your pensions into one of your employer-sponsored schemes

- Establish your own pension scheme called a self-invested pension plan (or a SIPP)

If you the take the first route, there could be the temptation to merge smaller pension pots into a big pension, simply because the smaller pension has less cash in it. But the same questions apply: just because this fund has the greatest value, is it the one that is most appropriately invested for your needs? And are its fees appropriate for the level of potential return? Depending on your circumstances, if the smaller fund has the better terms, you might actually be better off transferring out of the larger pot.

With the second route, SIPPs are recognised by HM Revenue and Customs as approved personal pension schemes so carry the usual tax benefits associated with saving into a pension. They are a personal contract between you and the pension provider rather than going through an employer.

Crucially, they offer much wider investment powers and allow you to make your own decisions about how your money is invested. They usually offer a broader choice of investment vehicles than an employer-sponsored plan.

However, the additional flexibility makes them more costly to administer and run and for this reason the fees and charges can be higher than other solutions. You will also have to select your own investments which you might not be comfortable doing without the help of a professional adviser.

The potential benefits

If you have several different pension pots, there are potential advantages to consolidating them into one. You:

- Can keep track of and manage your pension savings more easily

- Could save money if you transfer from higher-cost schemes to a lower-cost one

- Could access a greater choice of investments if you’re consolidating your pension pots into one flexible scheme.

- Could get a better idea of your retirement income, leaving you better prepared in case there’ll be less to live off than you think.

The downsides

There are potential downsides to watch for too:

- Do any of your existing pension schemes offer guaranteed annuity rates or a guaranteed minimum return? If they do, you should consider the implications carefully before transferring out. Even with the potential for future returns, you might not be able to match the income you could achieve by remaining in the scheme.

- Likewise, do they offer enhanced tax-free cash sums or other features?

- Will you be charged for transferring money out of a scheme? Some charge an exit fee expressed as a percentage of the value of the assets transferred.

- In general it’s a bad idea to transfer out of defined benefit or final salary pension schemes without taking professional financial advice. The guaranteed retirement income they offer shield you from investment risk and they can also offer a spouse’s pension as standard.

And, of course, choice brings complexity

Consolidating your pension schemes into a SIPP has the potential to provide you with a wider range of investment options. But this can seem overwhelming and you could end up making the wrong choices for the right reasons. For example, taking too much risk with the aim of achieving higher returns, or not taking enough risk for fear of losing money over shorter time periods.

Talking to a financial adviser can help you understand what could be realistic to achieve and the most appropriate ways of reaching your long-term aims.

Conclusion

So, is transferring everything into one easy-to-manage pension the way to go? If you’re lucky enough to be in a final salary scheme, it will almost always make sense to stay put.

But if you have any other type of pension – where success or failure depends on the performance of your investments - consolidation could be worth considering, depending on your circumstances. Keeping down fees and ensuring your money is invested as appropriately as possible could help ensure a more comfortable retirement.

There are advantages to switching your pensions but there are also pitfalls. The best course of action will depend on what kind of pension you currently have and how long you have until retirement. But transferring can also be complex, so it’s always best to speak to an adviser who can work out the best route to suit your individual circumstances and can help you consider a wider range of assets you could use in retirement.

Sources

(1) https://www.recruitment-international.co.uk/blog/2017/12/employees-staying-average-of-4-dot-5-years-in-a-job-finds-bps-world December 2017

(2) https://www.independent.co.uk/life-style/millennials-jobs-career-work-salary-quit-young-people-study-a8361936.html May 2018

(3) https://bandce.co.uk/lost-pension-pots/?_ga=2.138472435.1343588967.1579799474-385129956.1577971668 June 2018

Important information

Any views expressed are our in-house views as at the time of publishing.

This content may not be used, copied, quoted, circulated or otherwise disclosed (in whole or in part) without our prior written consent.

Fees and charges apply at Schroders Personal Wealth.

In preparing this article we may have used third party sources which we believe to be true and accurate as at the date of writing. However, we can give no assurances or warranty regarding the accuracy, currency or applicability of any of the content in relation to specific situations and particular circumstances.

Pensions are a long-term investment. The retirement benefits you receive from your pension plan depend on a number of factors including the value of your plan when you decide to take your benefits, which isn’t guaranteed, and can go down as well as up. The benefits of your plan could fall below the amount(s) paid in.

Forecasts of future performance are not a reliable guide to actual results in the future; neither is past performance a reliable indicator of future results. The value of investments, and the income from them, may fall as well as rise and cannot be guaranteed and the investor might not get back their initial investment.

Always seek a professional opinion as tax rules can be complex, depend on individual circumstances and are subject to change.

This article is for information only and is not a personal recommendation. If you are unsure about the suitability of an investment you should speak to an authorised financial adviser.