Why invest in the markets when interest rates are high?

We explain why the recent sharp rise in interest rates does not mean people should switch from investments to cash. We note that stock markets can provide long-term growth, savings rates could fall and trying to time the markets is difficult.

In December 2021, the Bank of England’s base interest rate stood at 0.1 percent. Today it is 5.25 percent and you can get interest of around 5 percent from easy access savings accounts (1).

As interest rates have gone up, the attractions of holding cash have risen with them, particularly as there is little threat to capital with cash accounts. Cash certainly has a role to play when it comes to setting aside funds for a rainy day. But for longer term goals there are benefits from investing in the stock market even when interest rates are high. Indeed at Schroders Personal Wealth one of our key principles is to invest for the long term.

Investing in the stock market can seem daunting for many of us, but here we outline three reasons to consider doing so.

1. Stock markets provide long-term growth

Diversified investment portfolios have historically shown higher long-term growth than cash, although investment returns aren’t guaranteed and you may get back less than you invested. By ‘diversified’ we mean holding a range of investments rather than putting all your eggs in one basket.

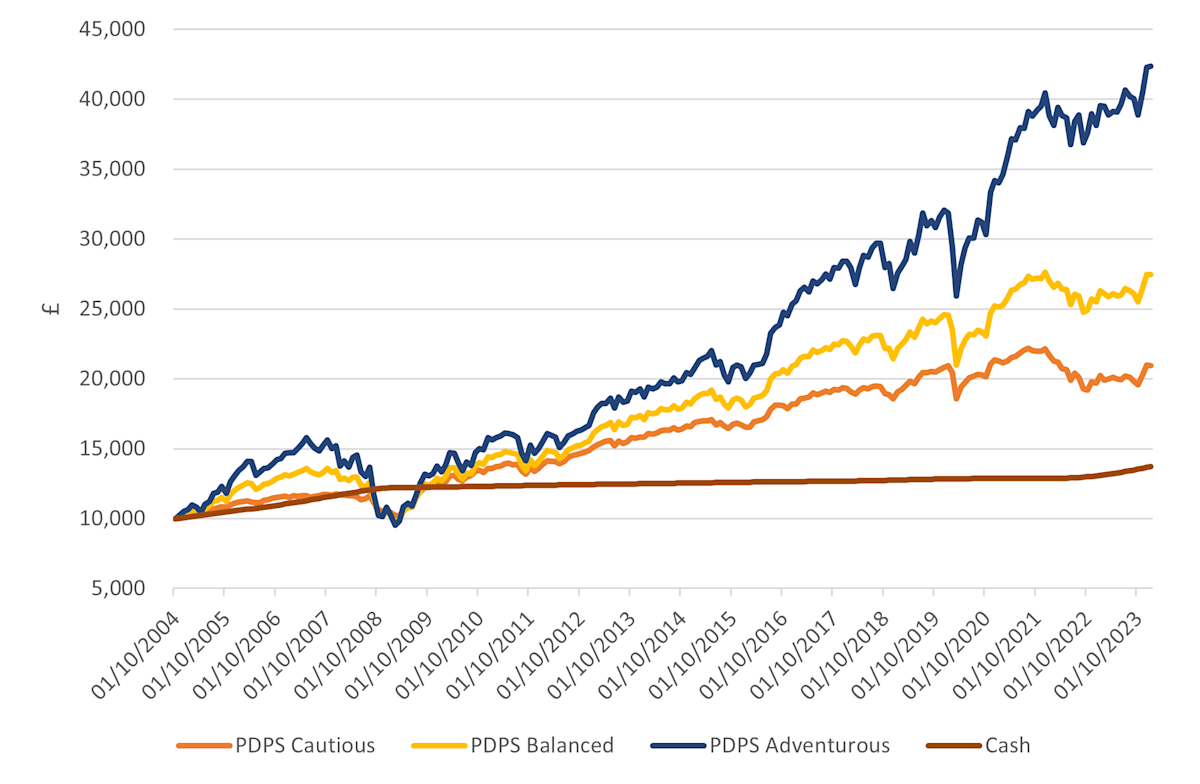

For example, all of SPW’s Personal Discretionary Portfolio Service (PDPS) profiles have performed better than cash since their inception in October 2004 (the chart below shows the performance of three PDPS portfolios against cash). But this does include a long period of ultra-low interest rates following the 2008 financial crisis.

How three SPW PDPS profiles have performed against cash since inception

2. Savings rates could fall

In February, Bank of England governor Andrew Bailey said inflation had ‘come down very rapidly’ in the UK. He added, ‘We don’t need … inflation to come back to [the 2 percent] target before we cut interest rates.’

Bailey has not said when the first rate cuts might come. But he said market expectations that the Bank would cut rates this year were not ‘unreasonable’. ‘I’m comfortable with a profile that has cuts in it, but that is not to say when or how much,’ he added (2).

These comments raise the prospect that UK interest rates could fall. And this would lead bank account savings rates to fall too, reducing the attractions of holding cash.

3. Timing markets is difficult

When stock markets are turbulent some people might understandably consider selling their investments and holding cash instead, with the intention of returning to the markets when they are calmer.

Unfortunately, switching between cash and investments in an attempt to time the markets is notoriously difficult, as ‘The cost of trying to time the UK market’ article shows. This article reveals that missing out on just a few of the best days of market performance can dramatically reduce investment returns. It can be very difficult to know in advance when these best days might be. That’s why at Schroders Personal Wealth we say investment is about spending time in the markets rather than trying to time the markets.

In short, while savings rates have risen sharply in the past couple of years, you will still need to invest in the stock markets if you require long-term growth. If you’re unsure about suitable investment options, you could consider speaking with a financial adviser. Advisers can offer support and insights to help you make informed decisions about your investments.

Sources

(1) moneyfactscompare.co.uk, ‘Best easy access savings accounts’, 12 March 2024.

(2) Financial Times (www.ft.com), ‘Bank of England may begin cutting rates before hitting 2% inflation target’, 20 February 2024.

Important information

This article is for information purposes only. It is not intended as investment advice.

Past performance is not a reliable indicator of future results. The value of investments and the income from them can fall as well as rise and are not guaranteed. The investor might not get back their initial investment.

Any views expressed are our in-house views as at the time of publishing.

This content may not be used, copied, quoted, circulated, or otherwise disclosed (in whole or part) without our prior written consent.

In preparing this article we may have used third party sources which we believe to be true and accurate as at the date of writing. However, we can give no assurances or warranty regarding the accuracy, currency or applicability of any of the content in relation to specific situations and particular circumstances.